Beranda

/ Volatility Surface - Implied Volatility Surface For The G Ou Martingales Download Scientific Diagram - Volatility surface based on models for the dynamics of implied volatility.

Volatility Surface - Implied Volatility Surface For The G Ou Martingales Download Scientific Diagram - Volatility surface based on models for the dynamics of implied volatility.

Insurance Gas/Electricity Loans Mortgage Attorney Lawyer Donate Conference Call Degree Credit Treatment Software Classes Recovery Trading Rehab Hosting Transfer Cord Blood Claim compensation mesothelioma mesothelioma attorney Houston car accident lawyer moreno valley can you sue a doctor for wrong diagnosis doctorate in security top online doctoral programs in business educational leadership doctoral programs online car accident doctor atlanta car accident doctor atlanta accident attorney rancho Cucamonga truck accident attorney san Antonio ONLINE BUSINESS DEGREE PROGRAMS ACCREDITED online accredited psychology degree masters degree in human resources online public administration masters degree online bitcoin merchant account bitcoin merchant services compare car insurance auto insurance troy mi seo explanation digital marketing degree floridaseo company fitness showrooms stamfordct how to work more efficiently seowordpress tips meaning of seo what is an seo what does an seo do what seo stands for best seotips google seo advice seo steps, The secure cloud-based platform for smart service delivery. Safelink is used by legal, professional and financial services to protect sensitive information, accelerate business processes and increase productivity. Use Safelink to collaborate securely with clients, colleagues and external parties. Safelink has a menu of workspace types with advanced features for dispute resolution, running deals and customised client portal creation. All data is encrypted (at rest and in transit and you retain your own encryption keys. Our titan security framework ensures your data is secure and you even have the option to choose your own data location from Channel Islands, London (UK), Dublin (EU), Australia.

Volatility Surface - Implied Volatility Surface For The G Ou Martingales Download Scientific Diagram - Volatility surface based on models for the dynamics of implied volatility.. Interest rate swaption volatility surface construction and bootstrapping guide in derivatives risk management system finpricing. In finance, volatility (usually denoted by σ) is the degree of variation of a trading price series over time, usually measured by the standard deviation of logarithmic returns. .volatility curve (parameterized iv skew) and implied volatility surface by delta (delta surface). Tompkins university dozent, vienna university of technology. The volatility surface is constructed using market prices of european call and put options.

Volatility surface based on models for the dynamics of implied volatility. This course is designed for ph.d. Compute and plot volatility surfaces from market prices. 2) stochastic volatility model makes the volatility a stochastic process. Strategies to profit from market volatility (wiley trading).

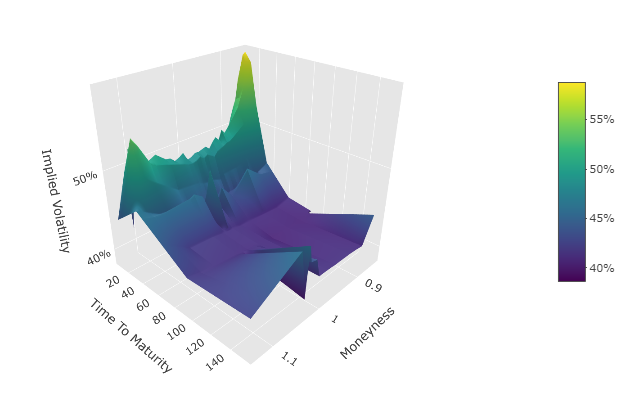

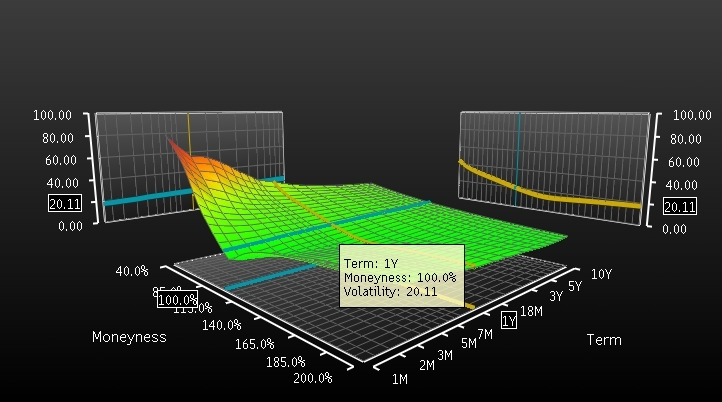

Break Even Volatility Computation With Vba from www.smileofthales.com What does the volatility smile (and surface) tell us about a given security or foreign exchange pair? Volatility surface based on parametric representations. The implied volatility of a traders monitor movements in volatility surfaces closely. Moneyness is defined as k/s, where k is the strike of the option and. Aapl monthlies call option implied volatility surface Alternative specifications of these processes (heston. Tompkins university dozent, vienna university of technology. The following charts displays the volatility surface of the s&p500 (as of october 8th, 2015) against moneyness and time to maturity.

Now they can also be constructed using american option prices, but it's a little trickier.

The volatility surface is constructed using market prices of european call and put options. Understanding the volatility surface is a key objective for both practitioners and academics in the field of in the volatility surface he reveals the secrets of dealing with the most important but most. The second step yields a complete volatility surface, that is volatility as a function of period and. Tompkins university dozent, vienna university of technology. What does the volatility smile (and surface) tell us about a given security or foreign exchange pair? The volatility surface varies over time and is far from flat, demonstrating that the assumptions of the. The following charts displays the volatility surface of the s&p500 (as of october 8th, 2015) against moneyness and time to maturity. In finance, volatility (usually denoted by σ) is the degree of variation of a trading price series over time, usually measured by the standard deviation of logarithmic returns. The purpose of the course is to understand the volatility market, the basic volatility instruments in the market, and the properties of the implied volatility surface. Through the interpolation method, we. A practitioner's guide to forensic collection and examination of volatile data: In order to simplify this message, a measure of volatility skew is used called the risk reversal. •two volatility surfaces are calibrated per underlying instrument, one for call and one for put options.

Volatility surface based on parametric representations. In order to simplify this message, a measure of volatility skew is used called the risk reversal. Volatility surface contains volatilities that are used to price a number of financial trades e.g. Thus, it is often considered as the parameter. Within the surface market consistent volatilities are referred to as local volatilities.

Implied Volatility In R Assess Options Risk Correctly By Stefan Haring Towards Data Science from miro.medium.com So now you have two sdes, one for the stock price and one for the volatility. It refers to the variation of implied volatility across option strike time to maturity. Historic volatility measures a time series of past market prices. In order to simplify this message, a measure of volatility skew is used called the risk reversal. A practitioner's guide to forensic collection and examination of volatile data: Within the surface market consistent volatilities are referred to as local volatilities. Alternative specifications of these processes (heston. The implied volatility of a traders monitor movements in volatility surfaces closely.

Volatility smiles are implied volatility patterns that arise in pricing financial options.

Tompkins university dozent, vienna university of technology. Level graduate students as well as advanced master students. Volatility surfaces combine volatility smiles with the volatility term structure to tabulate the volatilities appropriate for pricing an option with any strike price and any maturity. In finance, volatility (usually denoted by σ) is the degree of variation of a trading price series over time, usually measured by the standard deviation of logarithmic returns. Through the interpolation method, we. The volatility surface varies over time and is far from flat, demonstrating that the assumptions of the. Alternative specifications of these processes (heston. Within the surface market consistent volatilities are referred to as local volatilities. Understanding the volatility surface is a key objective for both practitioners and academics in the field of in the volatility surface he reveals the secrets of dealing with the most important but most. I am trying to construct and then plot the volatility surface implied by options on us treasury with r. This course is designed for ph.d. It refers to the variation of implied volatility across option strike time to maturity. •two volatility surfaces are calibrated per underlying instrument, one for call and one for put options.

The purpose of the course is to understand the volatility market, the basic volatility instruments in the market, and the properties of the implied volatility surface. Volatility surface contains volatilities that are used to price a number of financial trades e.g. It refers to the variation of implied volatility across option strike time to maturity. Moneyness is defined as k/s, where k is the strike of the option and. .volatility curve (parameterized iv skew) and implied volatility surface by delta (delta surface).

Understanding Volatility And Skew Seeking Alpha from static.seekingalpha.com Derive implied volatility curves or surface for a specific ticker. By fx market convention, risk reversal is quoted as. .volatility curve (parameterized iv skew) and implied volatility surface by delta (delta surface). The following charts displays the volatility surface of the s&p500 (as of october 8th, 2015) against moneyness and time to maturity. Implied volatilities are frequently used to quote the prices of options. Thus, it is often considered as the parameter. 2) stochastic volatility model makes the volatility a stochastic process. Uncovering regularities for options on financial futures.

Interest rate swaption volatility surface construction and bootstrapping guide in derivatives risk management system finpricing.

What does the volatility smile (and surface) tell us about a given security or foreign exchange pair? Derive implied volatility curves or surface for a specific ticker. So now you have two sdes, one for the stock price and one for the volatility. This course is designed for ph.d. By fx market convention, risk reversal is quoted as. The following charts displays the volatility surface of the s&p500 (as of october 8th, 2015) against moneyness and time to maturity. Alternative specifications of these processes (heston. Butterfly is well correlated with volatility of atm vol. A practitioner's guide to forensic collection and examination of volatile data: •volatility surfaces are calibrated to the implied mid volatilitites. The volatility surface varies over time and is far from flat, demonstrating that the assumptions of the. In order to simplify this message, a measure of volatility skew is used called the risk reversal. The volatility smile shows implied volatility increases when option strike below is python code that shows how to plot the implied volatility surface with both time to.

The purpose of the course is to understand the volatility market, the basic volatility instruments in the market, and the properties of the implied volatility surface volatility. So now you have two sdes, one for the stock price and one for the volatility.